The Strait of Hormuz crisis is not without precedent. COVID disrupted supply chains on a global scale. What sets today’s crisis apart from COVID?

COVID was highly disruptive, but largely temporary in its effects. Supply chains continued to function, albeit with delays. Capacity was strained, yet the underlying production infrastructure remained intact.

The Strait of Hormuz crisis is driven by war. War is different from a pandemic because it can destroy supply itself. Refineries, pipelines, and port infrastructure may be damaged or taken out entirely. This creates a longer-term supply problem, as production and logistics assets cannot be replaced overnight.

Pandemics tend to cause delays in demand and supply. War, by contrast, can result in a structural loss of supply.

Not every industry is affected equally by the Strait of Hormuz crisis. Does every company need to care?

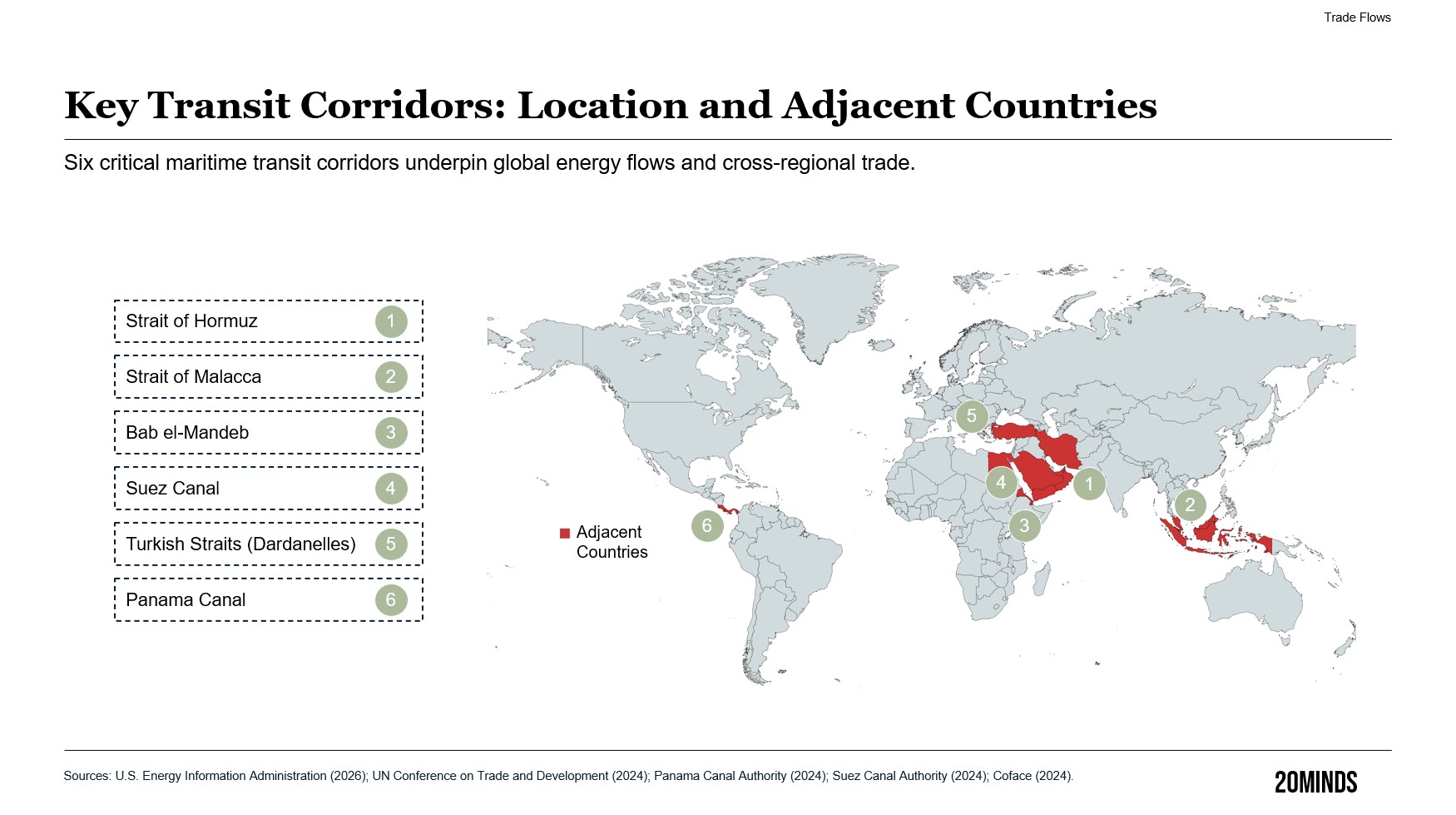

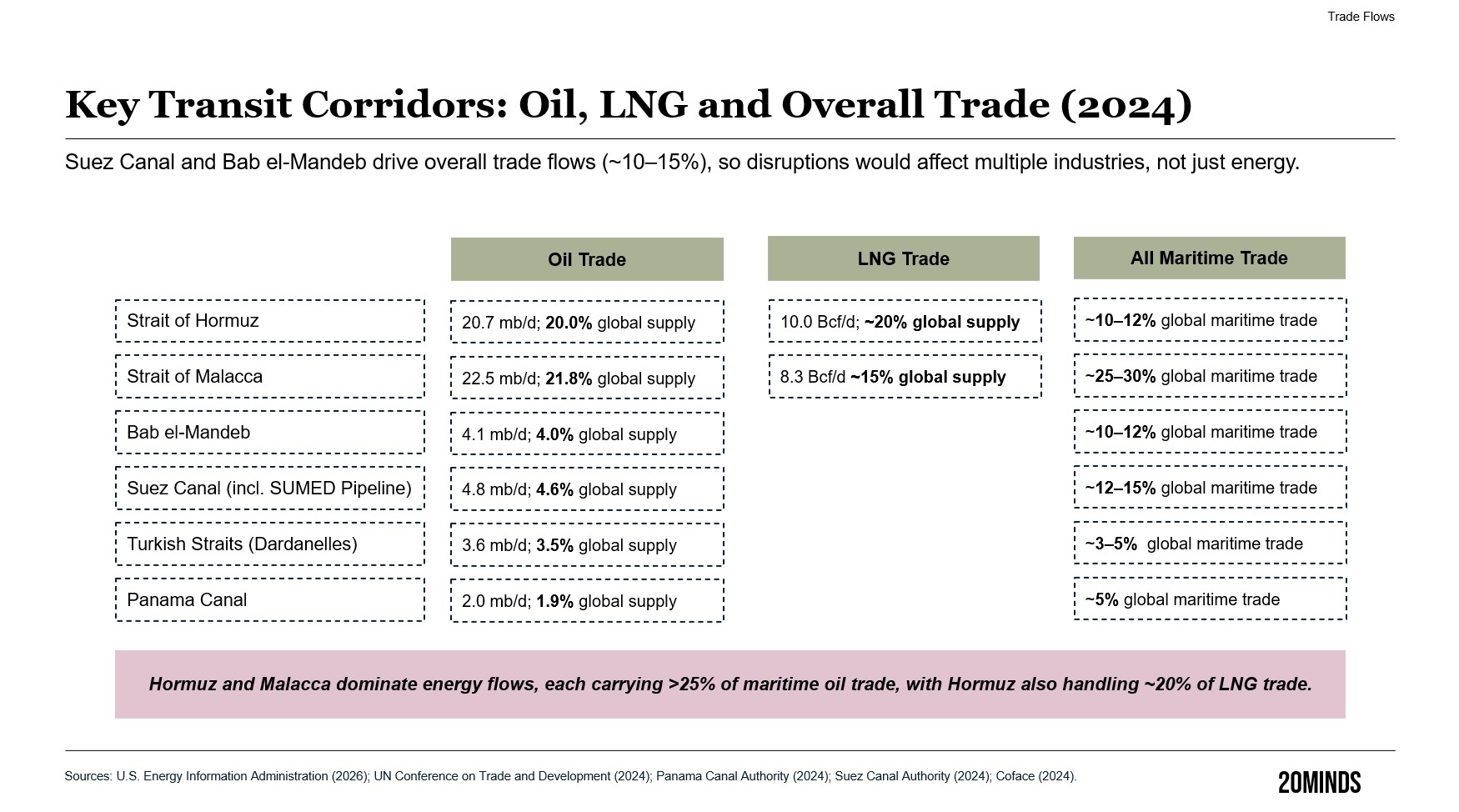

In my view, any business with global supply chains should assess how disruption would affect its supply chains—from an operational, legal, and ultimately financial perspective. As a practical first step, take a live disruption and ask a concrete question: which ships are currently delayed on disrupted routes in the Strait of Hormuz, and do we have cargo on any of them?

If not, then look further. A wide range of industries depends on energy or raw materials sourced from petroleum products in some form. Airlines, building materials, and the chemicals industry are particularly exposed to resource shortages.

Even if your company is not directly exposed to shortages, your supply chains could still be disrupted through transport bottlenecks, increased costs for any types of inputs or counterparties that are no longer able to perform. Your key counterparties and debtors may also be vulnerable to such supply chain shocks and your credit risk exposure to such parties may increase.

It is also advisable to consider how such disruptions may affect your customers. For example, could supply slowdowns on their end alter their demand for your services or products? (Ali Ahmad, 20Minds Editorial Advisor)

A useful starting point is a simple desktop exercise: what is the impact on us now, and what is the likely impact going forward? This already encourages a structured review of the exposure.

Besides the direct or indirect supply and logistics disruptions the strait of Hormoz conflict incur or may incur, the conflict may also create other indirect consequences for companies. There could be interruptions for the business of your customers in the region affecting their willingness to conduct new business or continue existing with your company. There could also be direct disruption on telecommunication and IT infrastructure in close proximity to the strait of Hormuz. (Per Hoffman, 20Minds Editorial Advisor)

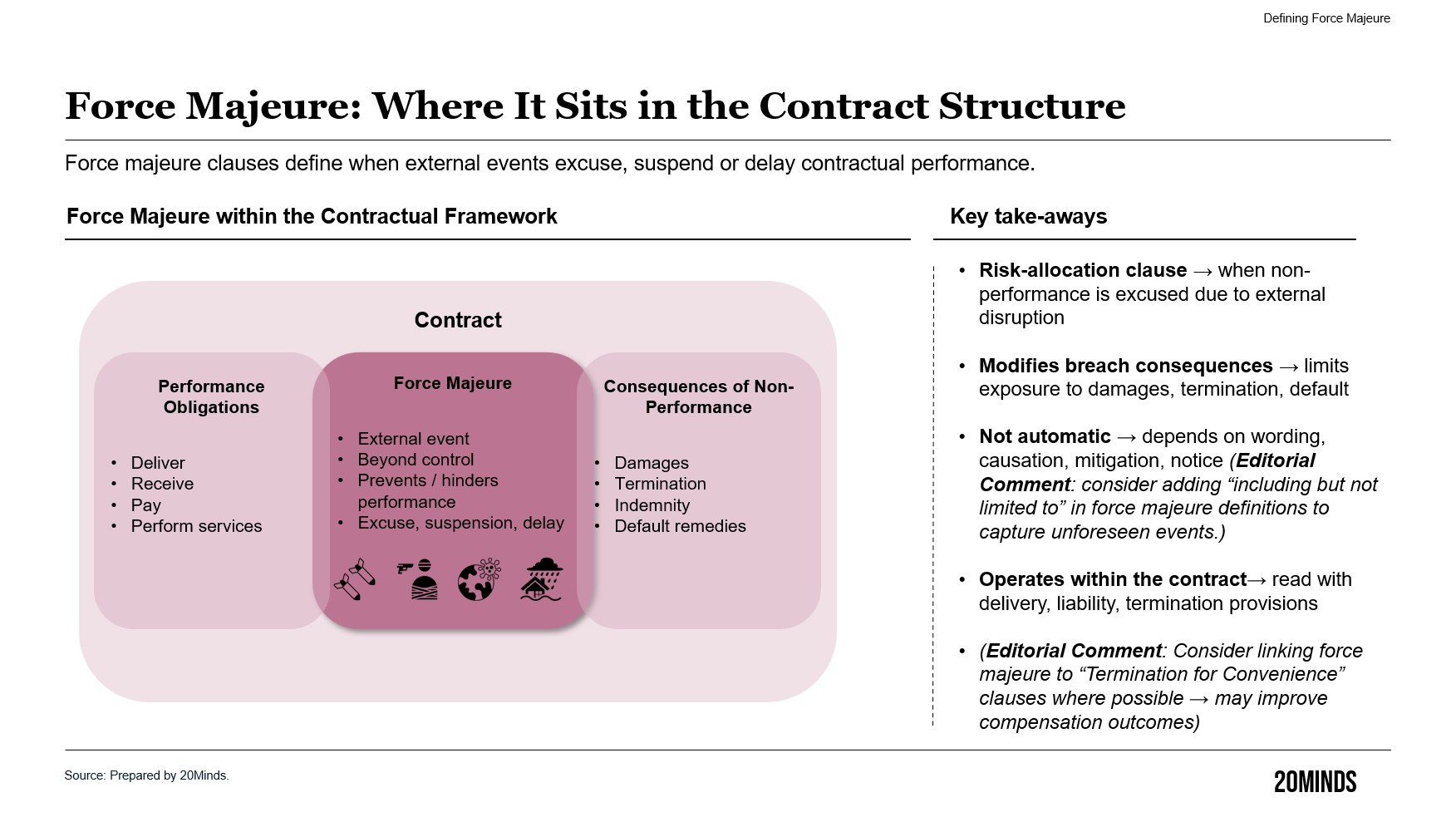

What is force majeure, and how do different models approach it?

Force majeure is a contractual mechanism that allows a party to suspend or excuse performance where an event beyond its control prevents, delays, or hinders performance. It may help the company avoid or limit liability for non-performance, and gain time to assess alternatives. Whether those benefits are available depends on the wording of the clause and the facts on the ground. There is no market standard force majeure clause and not all contracts will contain a force majeure clause: it is therefore important for the board of directors to instruct their General Counsel/ Chief Legal Officer to review the company’s material contracts impacted by the current crisis to see whether such contracts have such a force majeure clause and whether it can be of any assistance to the company when dealing with the current crisis.

Different model frameworks take distinct approaches:

- International Chamber of Commerce (ICC): The ICC Incoterms are the most commonly used set of model terms for international trade and provides a structured and widely used baseline for cross-border trades. The ICC has also produced a model force majeure clause, which defines a force majeure event as an event: (A) beyond the reasonable control of the parties; (B) which could not reasonably have been foreseen at the time the parties entered into the contract; and (C) the effects of which cannot be overcome by the affected party.

The ICC force majeure clause also lists specified events (including war) that are presumed to be force majeure events. If a war occurs, the ICC clause assumes that such an event is beyond the control of the parties and could not reasonably have been foreseen. However, the affected party must still demonstrate that it could not overcome the effects of the war.

- International Swaps and Derivatives Association (ISDA): ISDA documentation is commonly used to document privately negotiated derivative contracts including oil and petroleum derivatives. It uses the concept of Force Majeure Events within a broader termination framework. The focus is on whether performance becomes impossible or impracticable in financial markets. The primary consequence is often termination and close-out, rather than suspension. However, the ISDA Master Agreement does not specify whether war would constitute a force majeure event.

- BP (BP General Terms and Conditions 2015, Section 65): With BP as one of the largest oil producers in the world, the BP General Terms and Conditions are commonly used by international oil and gas traders and its model terms reflect the operational realities of the international petroleum market. It typically covers events that are impediments beyond the control of the parties prevent, hinder, or delay performance, including wars. The clause allows for suspension of obligations without liability while the impediment persists and may extend to obligations beyond delivery. It still places an obligation on the parties to mitigate and overcome the effects of the impediment and the party seeking to rely on the force majeure clause has detailed obligations to provide notice to the other party.

In practice, the outcome depends less on the label “force majeure” and more on how narrowly or broadly the clause is drafted—particularly in relation to causation, mitigation, and the consequences of non-performance. If there is no force majeure clause, the General Counsel will need to advise whether the governing law of the contract addresses this event. For example, if English law is applicable, the General Counsel will need to consider whether the legal principle of frustration would be applicable.

It is important to remember that force majeure is mainly a contractual principle, meaning that the choice of applicable law for the contract is important. For instance, in a contract under English law a specific force majeure clause must be included for any of the parties to be able to invoke force majeure. (Per Hoffman, 20Minds Editorial Advisor)

What methodology should the Board of Directors implement to address this risk?

While each company will be impacted by this crisis differently, the common requirement is that each company needs to have a methodology to assess the impact on the company and what steps can be taken to mitigate the impact.

Part of this methodology will require a cross-functional process across Legal, Operations, Finance and the Chief Executive Office that provides the Board with clarity on:

- which supply chains and inputs are affected;

- which underlying contracts are exposed;

- the likely financial impact and operational impact;

- Increase in credit risk impacting the company’s key suppliers and debtors;

- available mitigation options, including force majeure clauses exist; and

- how the company should respond in the immediate term and in the months ahead.

Ideally, this process is established and regularly updated before a crisis occurs. Without it, valuable time is lost before the company even understands where the problem lies.

At a minimum, the company needs a clear view of its contracts, the economic value they represent, and the force majeure mechanisms they contain.

One should also consider that force majeure may trigger termination of the contract after a specified period. The question remains how this termination is to be characterised, whether as termination for default or for convenience, which may have implications for costs and compensation, and which party has the right to invoke it. (Editorial Comment)

Decisions in a crisis often need to be taken quickly. How should the methodology help companies prioritise?

The methodology should focus on the most commercially significant contracts.

For those contracts, the immediate questions include:

- What are the delivery obligations and are they directly or indirectly impacted by the current crisis (e.g., inability of the ship carrying goods to transit through the Straits of Hormuz)?

- Does the contract include a force majeure clause? If so, does the clause cover war or similar hostilities? Does it require impossibility, or is hindrance sufficient?

- If the contract is silent, does the applicable law have a legal principle that would be applicable (eg the English law principle of frustration)?

If a relevant force majeure clause exists, what can still undermine the position?

Even where a clause appears to apply, a force majeure declaration may fail. Several factors can weaken the position:

- Foreseeability: Was the contract entered into before or after the crisis emerged? If after, the disruption may be considered foreseeable.

- Causal link: Did the disruption directly prevent performance? Delays or rerouting may not meet the required threshold.

- Mitigation efforts: Were reasonable alternatives explored? Increased costs alone will typically not excuse performance.

- Allocation of supply: If limited supply remains, was it allocated fairly among customers?

- Notice compliance: Was notice given in accordance with the contractual requirements, including timing and form?

So, the company is dealing with uncertainty as to whether a force majeure strategy will succeed.

Yes, and the methodology used by the company should help decide whether to declare force majeure or revert to other mitigation strategies often need to be taken under significant time pressure. This may require further triage as regards alternative mitigation options:

- Which contracts are closest to breach?

- Which contracts can be renegotiated?

- Which contracts are longer-dated and can be addressed later?

- Which contracts are critical, in terms of relationships, future business, and potential litigation?

The Executive Management and the Board may want to focus the review on contracts that cannot be renegotiated or where there is insufficient time to do so.

Once the mapping is complete, what else does the Board need to see?

Ultimately, the methodology needs to provide the Board with an understanding of the financial impact. It will want to know what the disruption means for the company’s bottom line.

The CFO’s role is to translate the disruption into a financial figure, or at least a range, using established accounting principles. The methodology will also need to provide the CFO with sufficient information to make a financial assessment. While the event may be unprecedented, the assessment will typically rely on familiar concepts such as impairment, provisioning, and bad debt analysis.

This requires input from across the organisation:

- Legal assesses contractual rights and exposure;

- Business and Operations assess operational realities; and

- Finance applies accounting frameworks to quantify the impact.

- Communications or external relations assesses the need for holding statements or announcements to the press.

The company may need to alert its shareholders or external auditors on the financial impact it will have on its audited financial statements.

Should the Board expect certainty?

No. There will often be uncertainty around:

- the success of a force majeure position;

- the availability of insurance cover;

- the feasibility of alternative solutions; and

- the duration of the disruption.

However, the methodology should provide the Board with well-developed scenarios combining operational, legal, and financial assessments. At a minimum, these scenarios should include:

- the legal position under key contracts, including the strength of any force majeure argument;

- the availability and cost of alternatives;

- the potential insurance response;

- the impact on project finance or export credit Insurance;

- the financial impact under different outcomes; and

- a forward-looking assessment if the disruption persists.

Supply disruption is not only a “real economy” issue. How does it affect financial positions?

If a company has borrowed on the assumption of delivering goods and generating revenue, an inability to perform may lead to covenant breaches and default events. Derivatives can also be affected. In normal conditions, derivative positions are typically rolled or closed before delivery. In a crisis, this may not be possible, and physical settlement risk can re-emerge.

20Minds thank Errol Bong and the editorial advisors for their candid observations.